DEALING WITH THE DENIAL

This narrative - so far - has told of the new Florida communities launched as well as the many other accomplishments of the company since 1962. It also has told the parallel story of the development of Marco Island and the permitting process.

Now the two stories come together again as Dad and I and everyone involved fight to overcome the blow and to rebuild the company.

SHOCK AND OUTRAGE

The denial was a shock of earthquake proportions and the effort to deal with its repercussions was a nightmare.

I am as proud of this episode in our corporate history as I am with any of the other achievements of the Mackle family.

Directors were immediately contacted and given the news. They assisted in formulating the company's response, a press release published the same day as the Corp's public announcement.

A Board meeting was scheduled for the next day.

The meeting was dominated by Jack Peeples who explained his understanding of the decision.

He went on to discuss the legal options that were available to the company.

The meeting focused on these issue.

I left the meeting to deal with the catastrophe that faced us.

THE MARCO OPTION PROGRAM

My paramount concern was the customer obligation - all others followed from there.

The contracts were clear. If we did not complete the promised improvements and deliver a deed to the property by the contract date we had to refund all moneys paid in.

The cash that had been paid in on those contracts - at the end of 1976 - was $77,155,000.

The moneys paid in - less selling costs - were still in the company - no dividends had ever been paid. But it was mostly in the form of land and other non-liquid assets. Our stated net worth at the beginning of 1976 was $$55,000,000 but our real net worth - if current values of the land asset for example was used - was much greater. But it was not cash. And it would take time to turn it in to cash.

The refund obligation was immediate.

And the customer impact went beyond Marco. There were tens of thousands of other contract holders in Deltona's other communities. If they believed that the company was in serious trouble they would cease making payments and possibly file suits to get their money - already paid in - back. Day to day operations depended on the cash flow from these payments.

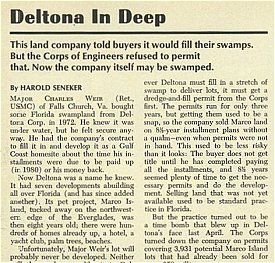

Six months later - in their October 1976 issue - Forbes magazine finally said in writing what we had all been thinking ..... and although Dad wrote a strong reply objecting to their conclusions .... they came pretty close to the truth.

Deltona In Deep!

There were things we could do however.

We thought that if we could hold off the demands for refunds or stretch them out over a long period of time there would be a chance that we could manage the situation. If we could manage the refund situation the bank problems, the regulatory problems, the sales force problems and the stockholder problems could be dealt with.

The phones in customer service - and all over the company - were ringing off their hooks. Every Marco customer and many other customers wanted to know what was going on. They were demanding their money back. Many were hostile. Many were threatening suit. Answers had to be given.

Within a day or two we had come up with a program which ultimately formed the basis on which the demand for refunds and all of the other company problems would be resolved - The Marco Option Program.

Most customers knew - and had been counting on the fact that - that developed property at Marco had appreciated in value far above their contract prices. So their disappointment was not only over losing the money they paid in but the current value of the property when - and if - delivered. They wanted their profits as well as their cash paid in!

Our obligation - as huge as it was - was still only for moneys paid in.

Deltona had thousands of platted unsold lots in other communities. Many were fully developed. They had also risen in value.

The Marco Option Program was based on two premises.

1. We were asset sound but we needed to "buy" time to liquidate assets to make refunds.

2. Customers who originally bought Marco lots might be willing to take other property or other non-cash solutions instead.

So the Marco Option Program gave the customer five options categories.

After explaining the company's situation - and our determination to make good on our contractual obligation - the Customer could opt for:

1. A refund to be paid over three years with interest paid from the date of the Corps denial.

2. Property in other communities exchanged on the basis of the prices as they existed on the date of original purchase. A few lots - mostly in the recently permitted, Collier Bay area, were available as well.

For example - if a Marco contract had been signed in 1966 for $10,000 and a lot in Deltona Lakes had been selling in 1966 for $2,000 the buyer could now swap his one Marco lot for five Deltona lots. And since the Deltona lot might now be selling for $3,000 some or all of his anticipated appreciation would be protected.

3. Transfer of the equity paid in on the denied lot to other property he was already on contract for. There were a number of multiple contract holders and - for them - this was an attractive solution.

4. Application of paid in moneys to home or condominium properties that the company had available. A discount from current prices was thrown in for good measure.

5. Or the contract holder could "do nothing" and wait for the results of the lawsuits and potential settlement proceedings that the company was pursuing. Some were willing to wait and see.

In order to actually pay the refunds - even over three years - the company had to face the fact that it must liquidate some of its prized lands and other assets. So we designated a large percentage of the remaining Marco beachfront and most of the Marco commercial core to be placed on the market.

The "family jewels" would have to go!

These properties were considered to be the "pot of gold at the end of the rainbow." They had never been put on the market either as land product or condo or commercial product. It was planned from the start that they should be reserved until the rest of the development had matured and the demand for them was maximized. They would also be the basis for investments in on-going operations - such as hotels and shopping centers - creating permanent revenue streams. The Mackles had seen what values they had created at Key Biscayne and other communities. The Key Biscayne Hotel and its adjoining, undeveloped land, for example, was now generating significant annual revenue and was worth many times what the entire project had sold out for in the 1950's. At Marco they would mine this vein of gold at a later date.

But no longer could we afford to do that.

Two years earlier the company had created Deltona Land and Investment Corporation (D.L.I.C.) with master salesman, Neil Bahr, as its President. Originally D.L.I.C. was formed to both acquire new land and also to dispose of excess land and specialty property not necessary for Deltona's basic business. Now the Neil was the primary cash generator for the company as he was given the most valuable lands - as well as the Marco Beach Hotel and other assets - in Deltona's inventory to sell.

Later, the company's promise to set aside those lands were not enough for the regulatory agencies and formal agreements to that effect were made with the state of Florida putting the lands into Trust.

So with the creation of the Marco Option Program the Customer Service representatives had some answers.

It did not solve all of the problems immediately. But it gave the customer something to think about. It was received - by reasonable people - as a fair - if not totally satisfactory - approach to the problem.

The phones were still ringing off the hooks. But now at least, it was because they were responding to or at least discussing the option program, being offered specific properties in exchange, being sent brochures on other communities as well as our home and condo products and discussing - sometimes trying to negotiate - the pros and cons of the program.

We had bought some time to solve the other problems weighing on us. And the fact of the program and its the general success was evidence for our bankers the regulators and our stockholders that everything that could be done was being done.

Of course - for some - the option program was not acceptable. Out of the 6,000 lots purchasers under contract a small percent went straight to their lawyers. Less than a few dozen suits were actually filed but more were threatened so the legal staff had their hands full dealing with each of them. Where suits were filed in other states outside counsel was hired.

The real concern in the area of lawsuits was that a class action be certified. A class action suit would ask the court to consider all of the contract holders as a single group and try the case for refund and perhaps other damages at one time. If such a class were certified it could not only suspend the Option Program but expose the company to the total refund obligation or more at one time. Class action certification attempts had to be fought or settled at all costs. No effort or expense was spared in such cases.

THE LAND SALES REGULATORY AUTHORITIES

Beyond the Customer problems there were major - potentially bankrupting - Regulatory and Bank Loan problems as well. Then there were the affects on the Sales Force and the rest of the organization and the impact on the financial community and - of course - our stockholders.

The company was registered for the sale of land in the federal Office of Interstate Land Sales (O.I.L.S.R. - often pronounced "olser" if not "ulcer") and perhaps three dozen state regulatory offices across the country.

Every one of them were there to protect their citizens. Every one of them wanted to know why their citizens were not threatened by the companies precarious financial condition. Every one of them wanted to know why they should not suspend our right to sell our Florida property in their jurisdiction. The Florida authorities were particularly aggressive and basically took the lead in assuring the state that purchasers were protected.

The heads of our Legal Department and Department of Regulatory Affairs made personal visits with virtually all of them. I accompanied them to the Florida, the New York and to the O.I.L.S.R. offices on their initial meetings after the denial.

One by one the regulators were carried through the history of the permit process, and what we were doing about the denial.

We explained our Option Program and the lands we had set aside to solve the problem. We explained that we had the backing of our lenders.

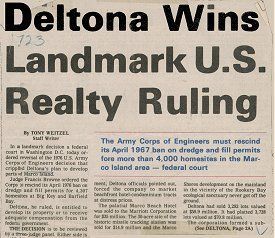

Eventually through discussions and negotiations Florida - with primary jurisdiction - agreed to let us continue to sell. They did extract significant concessions from us. The major one came in the form of requiring us to deed over the "set aside lands" to a trust with the affected customers as beneficiaries. Later as the denials squeezed the operating cash flow of the company and other project deliveries became delayed they began to hold us to specific delivery dates with suspension of our right to sell as a penalty for failing to meet those dates. These new demands that were put on us and the continuing cash flow problems caused us to constantly revisit the staff of the land sales board to modify or get extensions.

Once Florida had signed off on the Marco Option Program and the Marco Land Trust the other authorities pretty much followed suit.

At least we were still in business!

THE BANKS

At the end of 1976, the Company was still current on all debt obligation .... but things were getting very tight. Neil was gearing up to maximize bulk land and asset sales. Revenues from installment land sales were dropping as a result of lower Three Seasons sales and moratoriums and cancellations on Marco agreements. Condo and house sales were both down in 1976 resulting in further cash shortfalls. There was just so much you could do to cut expenses and we had already done what we could starting in 1973 and 1974.

Our Debt had been reduced slightly from 1975 to 1976 due primarily to the reduction in construction loans. At the end of 1976 It looked like this:

Mortgage and similar debt

Mortgage Notes Payable - $57,379,255

Revolving credit and security agreement and bank loans - $112,133,505

6 3/4 % Senior notes payable - $9,375,000

Construction and improvement loans - $11,145,909

6% Subordinated debentures - $4,063,674

TOTAL - $194,097,343

The equity in the company at the end of 1976 - after the first of what was to be several major reserves for the Marco situation - was $44,879,816 - resulting in a debt to equity ration of 4.3 - extremely high.

The Mortgage Debt, the Senior notes, the Construction and improvement loans and the Subordinated Debentures were part of the cash flow problem but they were all adequately collateralized as far as the issuers were concerned.

The primary problem arose in the Revolving Credit agreement. The Mackles - and their banks - had been pioneers in this form of loan. The good collection record of the company had persuaded the banks to accept the lot contract receivable as collateral. Now with the loss of the Marco receivable and the fear of increasing delinquencies in other communities and the general cash situation of the company the banks no longer felt secure.

The regulators had grabbed for their share of our land assets and the banks were simultaneously creating a tug-of-war for the same assets. Their Revolving Credit agreements gave them the right to demand land be put up as collateral and they were - at the beginning of 1976 - calling in that option. And the Revolving Credit Agreement had a four year term which was coming due on October 1, 1977. Further, the loan became a demand note as of May 30, 1977 until a new agreement could be negotiated.

So the banks had us by the throat.

And they were demanding the renegotiation of the other loan agreements as well!

The 1976 annual report - published in the spring of 1977 states:

"The Secured Loan Agreement, Revolving Credit and Security Agreement Revolving Construction Loan Agreement and the Secured and Unsecured demand loan agreements are currently being restructured."

An indication that cash was in short supply is revealed in the footnotes. Certain loan agreements required the company to keep 10% of the loan amount deposited with the banks as a "compensating balance" . When these balances were not met the loan was not in default but the costs of the loan increased so every effort was made to meet this provision. At the end 1976 we had a $7,050,000 shortfall in these accounts.

All through 1977 and early 1978 - well past the expiration of the Revolving Credit Agreement the company and the banks negotiated on a debt restructuring.

Finally on February 34th of 1978 a new agreement was in place. Footnote 5 of the 1977 annual report states:

"Principal collateral for the loans consists of a pledge of substantially all Company land inventories and land held for investment, bulk sale, or future development and certain property assets and any flow of funds generated from their disposition."

The only thing they didn't have a first lien against was the Trust Lands which had been grabbed by the State of Florida!

Further "putting our feet to the fire" the loan also set as an event of default certain debt reduction targets.

The State of Florida demands on the sale of Marco Trust lands to pay refunds and the pressure from the banks to repay debt at a time when operations were only just starting to turn around meant that we were in a major liquidation effort.

At least we were in control of the liquidation and not a Trustee appointed by the courts.

In the beginning there was no discussion of seeking protection from the bankruptcy court. Later when cash flow became critical and the banks were being stubborn we did seek advice from attorneys familiar with the process - for defensive purposes only.

But we were determined to avoid it at all costs. The fact is that a bankruptcy filing which left the creditor (us) in control might have been a financially better course. During the serious recession of the 1970s many firms chose just such a path. But the loser in such a proceeding would have been our customers, our banking relationships and ....candidly ... our reputation.

We never seriously considered that as an option.

And - although we were forced to the brink several times - we were successful in avoiding that alternative.

Over the next three or four years following the new loan agreement of 1978 there were constant renegotiations. As much emphasis as we put on asset sales the targets set by the bank were often not met. We were unable to meet all asset sales targets or make all required interest payments. While the banks were difficult they ultimately worked with us realizing that we were doing our best and the alternative of chapter proceedings was not in their interest.

Footnotes to the financial statements state that deferred, unpaid interest at the end of 1979 amounted to $17,849,000 and $18,989,000 at the end of 1980.

From the end of 1976 to the end of 1980 there was tremendous progress made in overall debt reduction - in spite of the shortfalls. The "problem" debt included Mortgage Notes Payable, the Revolving Credit Loan, the Senior notes payable and the Subordinated Debentures. Together they totaled $182,951,000 at the end of 1976. At the end of 1980 they were down to $92,527,000.

In 1981 - with the company's return to profitability and significant reduction of the "problem debt" - a new loan agreement was put in place whereby the remaining $14,978,000 of deferred interest was converted to interest paying debt and all interest payments were brought current.

We felt we had finally come out of our five year financial nightmare.

But - as the old saying goes - "the light we saw at the end of the tunnel turned out to be train heading our way."

As will be seen, a new crisis was about to occur as interest rates soared and the condominium business collapsed.

THE SALES FORCE AND THE ORGANIZATION

The loss of Marco inventory at the beginning of 1974 had already had it impact on the sales organization and the staff at Deltona. Franchised agents and Branch office representatives who had specialized on Marco and its higher income customers were virtually "out of business". Those that remained were further devastated by the denial. Now they not only had no product to offer, they were being inundated by calls from prior customers who were affected.

The obvious financial difficulties and the rumors of impending bankruptcy did not make the job of motivating the sales force any easier. The introduction of Tierra Verde product earlier in 1976 was a help.

There had already been massive cuts in Deltona staff in 1974 and 1975. Now the situation was even more critical and staff was cut again.

The good news was that those who were left were too busy to notice!

The Key people involved in solving real problems were Earl Cortright and Bill Livingston and . They and their staffs worked tirelessly in their respective areas to keep the fire under control.

As did everyone!

STOCKHOLDERS AND THE FINANCIAL COMMUNITY

The customers .... the customer's lawyers .... thirty or more land sales regulation offices .... the banks .... the sales force ... employees ...

.... and (oh yeah!) our stockholders and the financial community!

They needed to be communicated with as well.

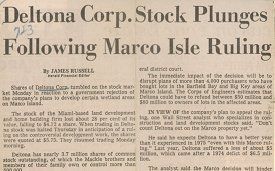

As so often happens the stock market seemed to have anticipated the bad news.

Deltona's stock price had been depressed since the recession of 1973. In the late 60s the price of the stock had been as high as $75 per share. The losses of 1974 and 1975 had depressed the stock as low as $2.75 per share.

In 1976 with a first quarter profit and a rebounding economy the stock price had crept back to $7.625. With the Corps announcement the stock sunk back below $5.00 again..... not too bad really.

But explanations had to be given. Stockholders and analysts had to be communicated with.

Our expression of "shock and outrage" was only a start.

How much financial damage had been done?

Everyone wanted to know.

The answers depended on the success of the Marco Option Program ... and of course the Lawsuits.

And neither result would be known for years.

So each year - as the year end statements were prepared - new estimates were made of the ultimate financial impact of the Marco Permit denials. Each year the auditors demanded and scrutinized our projections of cancellations, refunds and property swaps that would result from the Option Program. These numbers and other "crystal ball" forecasts of the overall and ultimate financial effect of the denial were summarized in a single line item called "Provision for Marco Permit Costs".

We were not very good at projecting the financial impact. We were always too optimistic.

In 1976 we concluded that an appropriate "Provision" would be $14,700,000.

The auditors were not totally convinced and "qualified" their opinion on or financial statements.

In 1978 we increased that to $20,400,00.

In 1979 we increased that again to $34,600,000.

And in 1982 we increased that - for the final time - to $58,300,000!

Finally the auditors were able to render a "clean opinion" as to our financial statements.

THE LARGER IMPACT

The Marco customers .... the Marco customer's lawyers .... the delayed Three Seasons deliveries ... the Three Seasons customers ... thirty or more land sales regulation authorities .... the banks .... the sales force ... the employees ... the stockholders .... the financial community ... the auditors!

It was a little like the vaudeville balancing act. If one thing went wrong everything would collapse.

Time and again "Dynamic Solutions" were found.

In time the multiple elements of the problem were under control.

But they continued to haunt the company in one way or another until the end.

And it was so costly!

The "Reserves" do not begin to tell the story.

The true impact was much much greater.

Lost were $28,400,000 in receivables from lots in the denied areas that would never be collected.

Millions more in deferred improvement revenues on those lots would never be recognized.

Lots still unsold in the permit areas at the time of the denial would never go to market.

And there were the lost "opportunity" costs!

There would be no profits from the thousands of acres in the master plans shown as "Future Development".

Lost forever were the opportunities that went with the liquidated assets.

The Marco Beach Hotel and its revenue and profit potential was lost - sold to Marriott to pay down debt.

Moreover the opportunity to add one or more new towers to the hotel and the profits they would generate were lost.

The opportunity to build our commuter airline was lost.

The opportunity for orderly development of much of the Marco Beachfront was lost - including the fabulous South Point.

Thousands of condominium units would be built by other developers.

The opportunity for orderly development of the Marco Commercial core was lost.

The opportunity to create new income producing businesses - new hotels - new shopping centers - with permanent income streams was lost.

The opportunity to generate revenue from valuable Three Seasons inventory lost through the Option Program was gone.

The opportunity to create another Three Seasons community in Polk County was lost.

Our sales force was devastated - setting back our recovery significantly.

Finally, even as we began to produce profits again - the condition of the company - still under capitalized - because of the staggering impact of the Corps of Engineers decision - was too fragile to deal with the new difficulties that emerged in the early 1980s.

SEEKING JUSTICE - THE TWO LAWSUITS

While the real corporate problems were being dealt with and solved others were "tilting at windmills".

That is not to say that I was not a supporter of the legal solutions being sought at the time. I hung on to the promise that those courses offered as much as anyone. But in the end the legal appeals produced nothing. At best the existence of them gave us hope and - in turn - we could give our customers some hope.

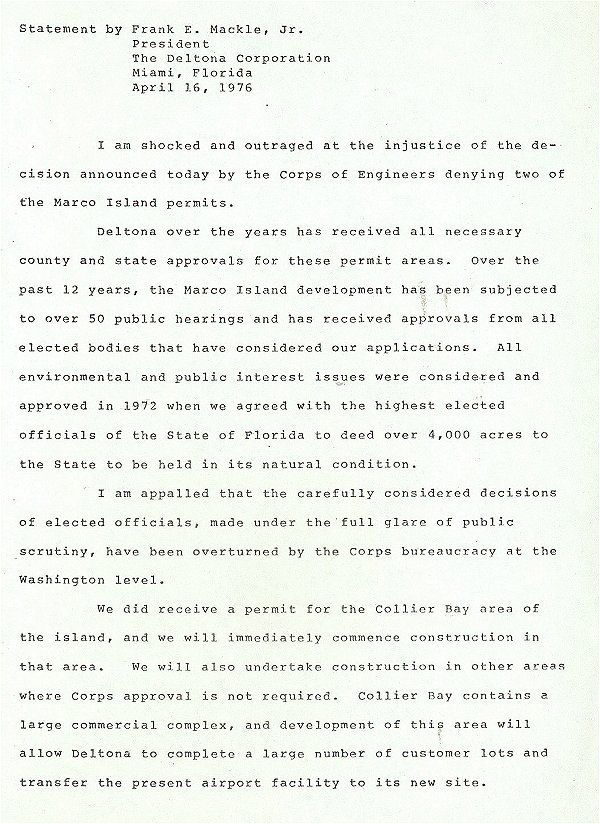

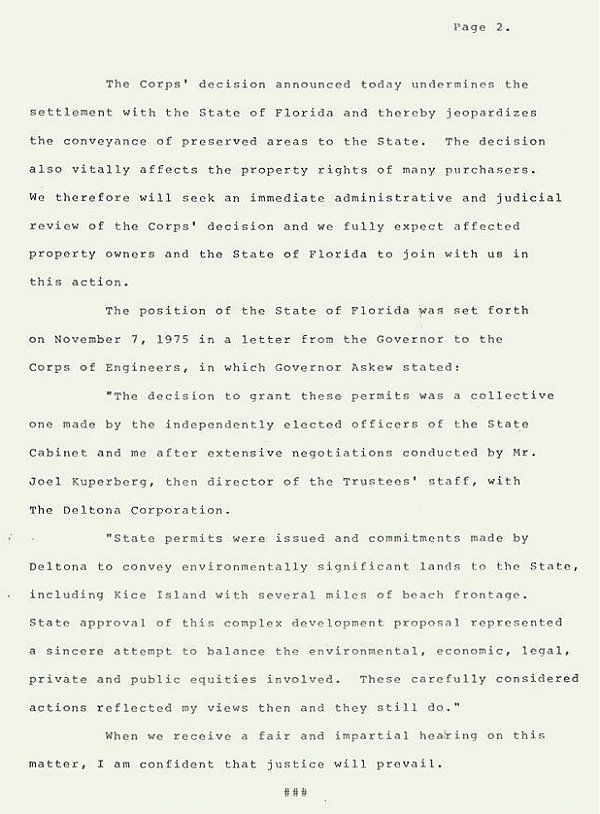

"When we receive a fair and impartial hearing on this matter, I am confident that justice will prevail" - Frank E. Mackle Jr. - April 16, 1976 press release

Dad and Jack Peeples truly believed that.... we all wanted to!

While Dad and Jack took the lead in pursuing them, the effort put an additional burden on our own people including myself.

Jack had left Deltona to form his own law firm in Miami. He took several of the young lawyers he had recruited at Deltona.

The firm was called Peeples, Earle and Blank.

Our Engineering, Environmental, Legal and other departments were called on to support their efforts. I became involved in the hearing in West Palm Beach before the Court of Claims.

For many years - a massive and expensive effort was under way to seek legal redress for the denial. There was no choice.

There were two legal courses taken - the Inverse Condemnation Suit and the Suit To Overturn the Corps Decision.

The Inverse Condemnation suit was filed in September of 1976.

The Inverse Condemnation Suit argued that the government - by denying Deltona the use of its lands - had "taken" the land as in a "condemnation" process. And - as such - the government was obligated to pay Deltona for the "taking".

There was precedent for such a suit although not in a case where a dredge permit denial was involved.

In 1980 the suit finally came before Judge Francis Browne in the lower division of the U.S. Court of Claims.

After all the filings and counter filings were done a week of testimony was scheduled.

The first day of the trial was set for the Courthouse in West Palm Beach. It was immediately obvious that the courtroom was not adequate.

Because of the public interest - and the huge number of experts expected to testify and the large volume of exhibits - a convention hall at a beachfront hotel on Singer Island was acquired for the trial.

The first phase of the trial would determine that a "taking" had occurred. If we were successful in that phase a second trial would be held to determine the "value" of the taking.

The first phase began.

We presented our arguments.

The government presented theirs.

There was so much more but - twenty or more years later - I remember one small part that seemed typical of the governments arguments.

They sought to demonstrate that Deltona still had an economic use for the mangrove swamp.

When they put on an expert who testified to the economic viability of a "monkey farm" in the mangroves I think the judge Browne began to "lean" our way.

In November of 1980 - four and a half years after the denial - Judge Browne ruled in our favor.

There had been a taking!

Unfortunately it did not end there.

The government appealed the ruling.

The appellate level of the Court of Claims - a three judge panel in Washington D.C. - with no public hearing - ruled two to one to overturn the lower court.

A year later - after presenting our motion for appeal - the Supreme Court of the United States refused to hear the case.

The Appellate ruling against us would be final.

The second legal strategy the Suit To Overturn the Corps Decision was was filed in the Middle District Court of Florida in November 1976.

The Middle District case had been suspended pending a final ruling by the Court of Claims.

In January 1981 the Middle District ruled in favor of the government.

The company filed an appeal.

In mid 1982 the Court of Appeals of the 11th Judicial Circuit affirmed the District Courts decision not to reverse the permit denials.

After six years of "seeking justice" ....

...... all legal remedies had been exhausted.

THE FINAL STATE SETTLEMENT

There was another course of action which sought some remedy.

Jim Apthorp, who for six years had been senior aide to Governor Ruben Askew, joined the company in February 1977 as Vice President and Special Assistant to the President.

Jim was a professional in the arena of the state government. Jims duties were many. He was involved in the lawsuits to some degree, the discussions with the regulatory agencies as well as the planning and permitting of new projects such as Tierra Verde and later Tampa Palms.

Most importantly he was the leader in an effort at a new State Settlement.

Jim had - prior to his term with the Governor been head of the Internal Improvement Fund of the State of Florida. And as Senior Aide to the Governor, Jim had been intimately involved with the 1971 State Settlement which the Governors office and the entire Cabinet had unanimously approved.

The State had, in fact, approved the Marco project at every level.

The argument began to be made that - in fairness - the state should give us permits on alternate properties as partial compensation for our loss.

This argument - while accepted by some - would never have seen the light of day except for one thing.

The environmentalists were not satisfied yet!

The denial had been historic in the movement's crusade to protect the wetlands. Assuming the decision withstood the appeals process never more would there be loss of mangrove or other wetlands to development anywhere in the U.S. It was hailed as just that kind of victory at the time and ever since mangroves have been virtually untouchable to developers.

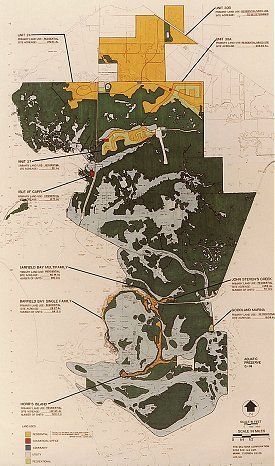

At Marco we owned 13,500 acres of mangrove swamp - in Big Key, in Barfield Bay, in Unit 24 and in - what the Master Plan called "Future Development" areas. This included the 4,000 acres which we had agreed to deed to the state if and when the final permits were issued. As far as we were concerned - unless the decision was overturned - none of the properties could ever be touched.

Nonetheless we still had title to them. And the environmentalists - for whatever reason - wanted them.

So a long and involved negotiation began with the concept that we would deed over the swampland to the State in exchange for new development rights and permits on the uplands.

The only problem was that we owned very little "uplands".

There was Horrs Island, a beautiful but tiny spit of land south of Marco Island. And there was a fringe of uplands on the north edge of Marco Shores. But it was not enough to design a project on.

So we set out - in spite of the cash shortage - to tie up through options and contingent contracts additional lands contiguous to the Marco Shores uplands.

We eventually accumulated about 3,000 new acres there.

As the negotiations proceeded and the concept began to be accepted we became aware of a piece of land in Dade county that the State had access to. We began to include that in the discussions as well.

The deal finally came together.

On March 24, 1985 a signing ceremony and press conference took place at the Conservancy Nature Center in Naples, Florida.

Governor Bob Graham - who had succeeded Governor Askew - and I signed the Final State Settlement.

The 1985 Annual Report Footnote 9 summarizes the State Settlement and subsequent events.

"On July 20, 1982, the Company entered into an agreement with the State of Florida and various state and local agencies, endorsed by various environmental interest groups, to resolve pending litigation and administrative proceedings relative to the Marco permitting issues."

"On September 29, 1983, the Company received a Corps permit to develop Marco consistent with the Settlement Agreement, and on January 19, 1984, the Company received a U.S. Coast Guard permit - the last remaining federal permit needed to complete development of Marco. The Settlement Agreement and the federal permits provide for the Company to develop as many as 14,500 additional dwelling units in the Marco vicinity. The Settlement Agreement became effective in March, 1985 when, pursuant thereto, approximately 12,400 acres of the Company's Marco wetlands were conveyed to the State in exchange for approximately 50 acres of State-owned property near the Miami International Airport in Dade County, Florida. The Settlement Agreement constitutes the permits required from the Florida Department of Environmental Regulation ("DER") for the development of the additional dwelling units in the Marco vicinity. In June, 1984, Collier County issued a development order and the Company obtained the remaining local approvals necessary to develop Marco Shores, Horr's Island and additional dwelling units at Marco island, in accordance with its application."

It was a settlement.

12,400 acres in exchange for 50 acres and some development permits.

It did not make a dent in the damage that had been done.

But it was the best we could do in the end.

The pursuit of "justice" was over.

As will be seen - we were never free of the burden of the Marco denial. Cash flow was tight until the end. When - in the early 1980s - other difficulties arose, we were still in a financially weakened condition which made matters that much worse.

Deltona's Customer Service Department continued to work out each and every individual contract - long after we left Deltona.

In 1997 - thirty two years after the first permit area lots were sold - twenty one years after the denial - eleven years after Dad and I left Deltona - I ran into Sharon Hummerhelm, who had been with Deltona - primarily in the Marco customer service area - since the Option Program had been created.

Sharon told me that the last Marco customer affected by the denial had just been paid off!

I congratulated her.

WHAT WAS ACCOMPLISHED

We met or exceeded all contract obligations.

We protected the investments of all 6,000 customers affected by the denial.

We - in most cases - preserved much of their hoped-for appreciation.

We avoided class action certification.

We delivered all other development promises.

We kept all registrations active.

We repaid or brought current all bank debt.

We emerged again as a viable company.

We successfully negotiated the Final State Settlement.

We avoided bankruptcy.

We returned the company to four years of profitability.

We brought the stock back from $2.75 per share to over $19.00 per share in 1981.

We lived up to the principles laid down by my granddad Frank Mackle Senior.

Governor Graham & I sign State Settlement Agreement